Atlantic Ave Beach

Amagansett

Sitting in Paton Miller’s home studio, a large warehouse-like building on the outskirts of his Tuckahoe Lane property, Paton led me through the adventures that allowed him to arrive right where he is today. Having grown up in this studio myself, from taking drawing classes as a child with Paton and running around their once-swimming-pool-now-turned-koi-pond with his youngest son Christian, it’s shocking to me that I never knew the tale that is Paton’s life story. So, let’s start from the beginning together.

Heiberg Cummings Design’s luxurious new construction home—Osprey House—is a one-of-a-kind architectural masterpiece delivering unmatched luxury and verve to the Hamptons. Located on Shelter Island’s picturesque Smith’s Cove, Osprey House epitomizes the unique blend of elegance, comfort, and innovative design Heiberg...

The Dining Room,” by A. R. Gurney, will be presented from April 26th through Sunday, April 28th at the Southampton Arts Center, located at 25 Jobs Lane in Southampton Village. There are numerous reasons to see this show.

Over the past week there were 25 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year (2023), there were 34 Listings that went into contract. Which is a year over year DECREASE of 26%. This same week in 2022, there...

Everyone loves a good happy hour menu, and when I heard about Shippy's version in Southampton, I had to go see it for myself. Every day from 3pm to 6pm, you can indulge in $7 wine, draft beer, and house...

BCM Spring, the annual series from Bridgehampton Chamber Music, Long Island’s longest-running classical music festival, welcomes spring in 2024 with two concerts, including a delectable French repertoire and Mozart gems featuring some of the finest chamber musicians performing today. The...

South Fork Bakery presents The 2nd Annual East End Bake-Off: Competition With a Cause - Birthday Cupcake Extravaganza, celebrating South Fork Bakery's 8th Birthday, on Sunday May 5, 2024. South Fork Bakery presents The 2nd Annual East End Bake-Off: Competition...

Heidi Humes, owner of lifestyle boutique SUNSHINE, has moved her coveted store to a brand new location in East Hampton. Formerly in Amagansett, SUNSHINE beams for having special items handmade by female global artisans around the world. There is a...

The Hamptons Whodunit Kick-Off Cocktail Party at the exclusive Maidstone Club in East Hampton on April 11th, a sold-out affair against the stunning backdrop of dunes and the golf course. Amidst the coastal breeze, guests, VIPs, sponsors, and donors mingled...

Looking for a summer camp for your little one? The search is over! Hamptons.com has curated a guide of the best camps in the Hamptons! From theater to sports, there are a variety of camps that your kids will love.

Montauk Brewing Company, the leading and fastest-selling craft brewer in Metro New York known for its exceptional craft beers, today announced the return of Project 4:20 India Pale Ale, a limited release crafted to celebrate and support green charities during...

Check out the top hamptons events this weekend!

Ashley Flowers was born and raised in Indiana, and she lived there with her family. She held a Bachelor of Science from Arizona State University and was the #1 New York Times Bestseller of the book All Good People Here....

Twelve years and still dancing! This weekend’s 12th Annual artGroove at Ashawagh Hall this Saturday and Sunday for a vibrant atmosphere in support of critical Hamptons charities. If you love dancing, supporting charities, or great Hamptons art—this is the weekend...

Over the past week there were 18 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year (2023), there were 22 Listings that went into contract. Which is a year over year DECREASE of 18%.

Sitting in Paton Miller’s home studio, a large warehouse-like building on the outskirts of his Tuckahoe Lane property, Paton led me through the adventures that allowed him to arrive right where he is today. Having grown up in this studio...

LTV Studios is celebrating its 40th year and has a wonderful roster of events planned. One coming up this weekend is of the South Fork Performing Arts, a 501c3 nonprofit youth performing arts education company. This weekend, at LTV Studios,...

“Multi-tasking is a mother’s domain,” Tahlia Miller smiles knowingly. In the time I spent with Lisa Fox and Tahlia Miller, now The Miller Fox Team, you can see how busy—but focused—they are. Both mothers who raised their families in the...

Live theater creates magic. The moment the curtain rises, the lights go up, and the music starts, the audience begins a journey of drama, comedy, music, or all of the above. Often, the venue itself adds to the whole experience,...

For many, a trip to the Hamptons is incomplete without a stop at The Clam Bar. As you drive east on Route 27, the anticipation builds. The cool ocean breeze caresses your face as you lower your car windows. The...

I remember being blown away by Mr. No Shame's performance at the iconic Stephen Talkhouse. The Latin drumbeat made everyone's feet move, as did the groovy electric piano and electrifying guitar riffs, all coming together under the potent, vibrant vocals...

So many fun events this weekend in the Hamptons! Check out the full list here!

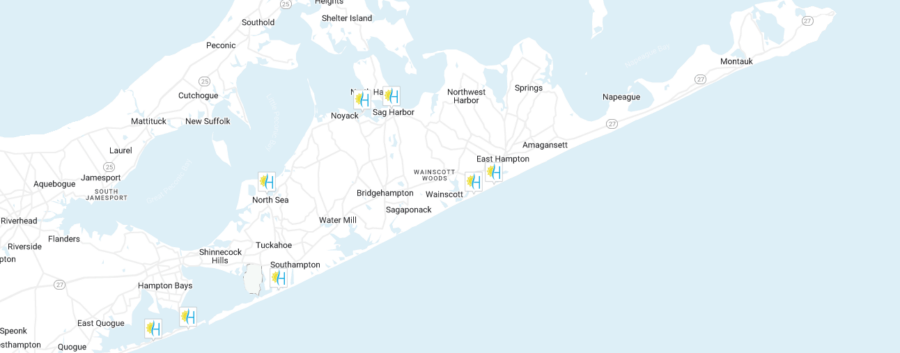

Over the past week there were 23 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year (2023), there were 15 Listings that went into contract. Which is a year over year INCREASE of 53%. This same week in 2022, there...

Heiberg Cummings Design’s luxurious new construction home—Osprey House—is a one-of-a-kind architectural masterpiece delivering unmatched luxury and verve to the Hamptons....

Read moreOver the past week there were 25 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year...

Read moreOver the past week there were 18 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year...

Read more“Multi-tasking is a mother’s domain,” Tahlia Miller smiles knowingly. In the time I spent with Lisa Fox and Tahlia Miller,...

Read moreOver the past week there were 23 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year...

Read moreIn the picturesque setting of Southampton, Naiztat + Ham Architects (NHA) has once again proven their unparalleled ability to blend...

Read more

.

.

.

.

.

#hamptons #shelterisland #realestate #saunders #design #cummingsdesign")

.

.

.

.

.

.

#montaukbrewingcompany #ale #craftbeer #montauk #earthday #hamptons")

.

.

.

.

.

.

.

#art #artist #patonmiller #southampton #local #hamptons")