Atlantic Ave Beach

Amagansett

Everyone loves a good happy hour menu, and when I heard about Shippy's version in Southampton, I had to go see it for myself. Every day from 3pm to 6pm, you can indulge in $7 wine, draft beer, and house cocktails and enjoy an assortment of $7 appetizers and bites. The hot German pretzel served with specialty beer cheese brought me right back to Oktoberfest in Munich.

Grammy award-winning singer, composer, and multi-instrumentalist LAUFEY will perform for one night only to benefit the Montauk Historical Society on August 3rd at the Montauk Point Lighthouse. The event will be produced by the New York-based events company Murmrr Presents....

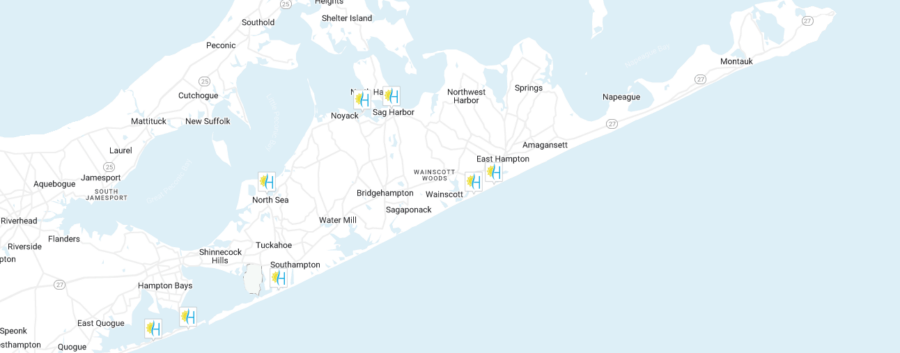

Over the past week there were 25 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year (2023), there were 24 Listings that went into contract. Which is a year over year INCREASE of 4%.

All The Summers In Between takes place in the Hamptons and in a dual timeline format. Moving between the years 1967 and 1977, the novel chronicles main characters Margot, the classic wealthy summer girl, and Thea, a “hardworking and steady...

I’m always looking to help highlight hidden Hamptons gems for rent, so when Jeanmarie told me she had a great waterside rental, that was just reduced for the Summer - I was surprised and intrigued. After visiting 4 Peconic Road...

Farm Day Camp at Fireplace Farm, Springs is a premiere educational experience for kids that combines getting involved with farming, an immersive nature experience, and art and playtime, all of which are essential for development and embracing the fun of...

Folks come to the Hamptons on trains, planes, cars, buses, and boats. Others have always lived here, while many wish they did. Its spectacular natural beauty amplifies the essence of being able to appreciate beaches, sunrises, sunsets, full moons, and...

Luxury, female-founded pajama and loungewear brand, Eberjey together with their fiber partner TENCEL™, hosted an immersive three-day wellness retreat at Shou Sugi Ban House in the Hamptons, bringing together powerful women, celebrating Mother’s Day and the wonderful mom and daughter...

Cinco de Mayo is this Sunday! You know what that means?! Margaritas, guacamole, and chips for the whole table! Check out the top spots in the Hamptons to celebrate in style.

The Trailblazing Women of Country is a dazzling, country-fried tribute to Patsy Cline, Loretta Lynn, and Dolly Parton that will be hitting the stage at the Westhampton Beach Performing Arts Center on May 5 at 8pm. Helmed by Miko Marks,...

Gear up for a weekend brimming with fun, from a thrilling baker-off to the exhilarating May Day 5K! There is something for everyone!

Shelter Island’s iconic Two Hearths Estate, located at 15 West Neck Road, masterfully refreshed over 10 years of restoration, stands as an enduring example of Greek Revival architecture here in the Hamptons. One of the four original Greek Revival homes...

Stop and smell the art! May is upon us, and the beginnings of a summer full of beach days, art openings, strolls on Main Street, and the energy only east-end goers know are in our future. We have all the...

One day, my friends and I started to talk about lunch. We all pitched different options like chicken fingers and quesadillas, but once pizza was mentioned, we all paused and said La Capannina? We were all in agreement; we cruised...

Even in the quaint streets of East Hampton, miles away from the nearest college, March Madness was alive and well. If not, maybe as “mad” as in college towns, Bonackers still honor the spirit of the games. I started catching...

Over the past week there were 18 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year (2023), there were 33 Listings that went into contract. Which is a year over year DECREASE of 45%. This same week in 2022, there...

As you might have noticed, in the past few years, interior and exterior design and decoration have been marked by whites and neutrals. The "Clean Girl" aesthetic took the internet by storm in 2022 and 2023, furthering this push towards palettes...

Looking for a summer camp for your little one? The search is over! Hamptons.com has curated a guide of the best camps in the Hamptons! From theater to sports, there are a variety of camps that your kids will love.

For coffee lovers, there’s nothing quite like heading into a local coffee joint, taking solace in the fact that it’s not an international chain. Quaint vibes alongside java that is brewed fresh and local is an experience that simply can’t...

Maidstone (Inn) Hotel and restaurant in East Hampton was reportedly sold for more than $12M last year and is scheduled to open on June 17 this Summer. When it reopens this season, it shall be under the new vision of John Meadow and...

Without a doubt, this is serious theater. It delves into behavior and subject matter that provoke thoughts about dark topics and subjects. Playwright Martin McDonagh reportedly said about this play, “…It’s about making violence as horrible as possible, and to...

The Hamptons is known for its beautiful landscapes and stunning beaches. Hamptons.com has curated the ultimate beach list! Pack up your umbrella, towel, and beach chair and enjoy a beautiful day in the Hamptons!

The Clubhouse to Host KK Strong Fundraiser in Support of Kayla Kearney On Saturday, May 11th, from 6:00 – 9:00 p.m., The Clubhouse in East Hampton will host a meaningful fundraiser to the Hamptons community in support of Kayla Kearney...

Over the past week there were 25 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year...

Read moreI’m always looking to help highlight hidden Hamptons gems for rent, so when Jeanmarie told me she had a great...

Read moreShelter Island’s iconic Two Hearths Estate, located at 15 West Neck Road, masterfully refreshed over 10 years of restoration, stands...

Read moreOver the past week there were 18 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year...

Read moreHeiberg Cummings Design’s luxurious new construction home—Osprey House—is a one-of-a-kind architectural masterpiece delivering unmatched luxury and verve to the Hamptons....

Read moreOver the past week there were 25 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year...

Read more

.

.

.

.

.

.

.

.

.

#nbaplayoffs #cittanova #hamptons #dining #easthampton")

.

.

.

.

.

.

.

#arts #easthampton #hamptons #exhibtions #localart #artist")

.

.

.

.

.

.

.

#flower #hamptons #pink #color #interiordesign")

.

.

.

.

.

.

#cincodemayo #margaritas #mexican #chips #mariachi#")

.

.

.

.

.

.

#events #hamptons #weekend #kentuckyderby #bakeoff #whbpac #5k #spring #springfling #lifeguard")

.

.

.

.

.

.

.

.

#benefit #local #fundraiser #kkstrong #easthampton #community")