Main Street

Westhampton

Empire of the Atlantic is a breathtaking taste of what everyone loves about the magic of the waters off the East End, specifically Montauk. Jeff Ragovin, Founder and CEO of Ragovin Ventures, is the executive producer through Bounty Uncharted Productions and assembled a team to bring the project to fruition.

ID Hot Yoga has quickly become a go-to destination for movement and mindfulness in New York City and on the East End, offering a modern, high-energy take on traditional yoga. Co-founded by Kelly Isaac and Tricia Donegan, the studio blends heat,...

Over the past week, there were 30 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year (2025), there were 23 Listings that went into contract. Which is a year over year INCREASE of 30%.

On April 18th, rain or shine, the Fourteenth Annual Katy’s Courage 5K will be held in Sag Harbor. On race day, registration and check-ins will take place from 7am to 8:15 a.m., and the run will begin promptly at 8:30...

A masterclass in architectural restoration and design, The Van Brunt Home is a rare convergence of timeless elegance and modern refinement. This meticulously reimagined, newly built Queen Anne residence pays homage to its storied Hamptons heritage and provenance while embracing...

2025 Long Island Restaurant Week: Spring Edition starts on Sunday, April 27th, and ends on Sunday, May 4th. Enjoy delicious 3-course meals at your favorite restaurants on Long Island. Check out the list below and plan the perfect dinner date.

Charlie Fox is the first Hamptons dispensary to fully lean into correcting cannabis misunderstandings and helping its customers ease into the experience. Charlie Fox allows you to book an appointment (in-person or online) with their experts to pair each p

Discover unparalleled new construction luxury located South of the Highway in East Hampton Village at 73 Jericho Road, a prestigious haven for elegance and comfort. Built by Konner Development and sited on a shy acre, this property offers 7,442 +/-...

For decades, Ross School has reimagined the educational experience, blending interdisciplinary learning, global awareness, and creative exploration into an academic setting on the East End. Founded in 1991 on the belief that education should reflect the complexity of the world, the school’s...

This property is available for the US Open this year. Private and quiet, set back approximately 340 feet off Noyack Road. Experience great summer living in this contemporary home bathed in sunlight, featuring an expansive lawn and a large deck...

Check out the top Hamptons events this April weekend!

The Happening in the Hamptons Podcast by Saunders & Associates is a weekly discussion covering all things Hamptons — from local events to in-depth real estate market analysis. This week, Augie Hoerrner joined and discussed the U.S Open Golf Championship.

The Hamptons Festival of Music (TH•FM) will present Viennese Voices on April 23, a special benefit concert designed as an intimate prelude to the orchestra’s Fifth Anniversary MainStage Season. The program highlights the Viennese lineage that shaped the symphony — a...

Looking for a commercial property with unmatched visibility in the Hamptons? This 0.92-acre fully renovated site sits on County Road 39, one of Southampton's busiest corridors, where every car traveling in and out of the Hamptons passes by.

Let’s be honest—there are two types of people in the Hamptons: those who go to Goldberg’s, and those who are wrong. By 8:30 a.m., the line is already forming, a mix of locals, contractors, summer people, and at least one...

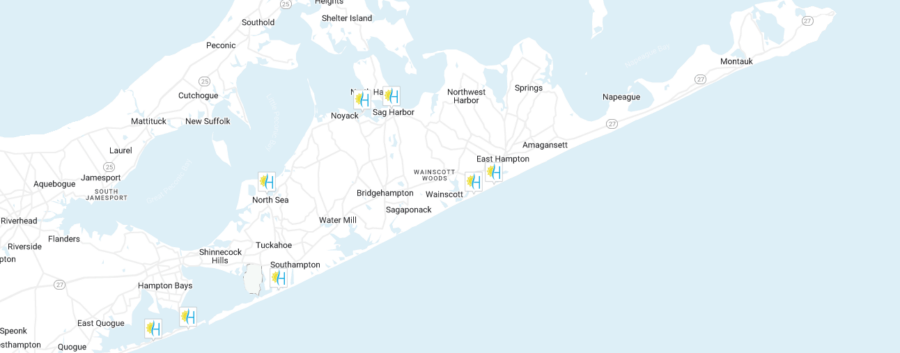

Over the past week, there were 18 Listings that went into contract from Westhampton to Montauk. Compared to this same week last year (2025), there were 31 Listings that went into contract. Which is a year over year DECREASE of 42%.

Looking for a summer camp for your little one? The search is over! Hamptons.com has curated a guide of the best camps in the Hamptons! From theater to sports, there are a variety of camps that your kids will love.

A modern residence located at 24 Rocky Point Road in Shelter Island’s estate section of Greenlawns, represented by Penelope Moore, Licensed Associate Real Estate Broker with Saunders & Associates, is offered for sale and has just been re-priced to $3,290,000...

Philanthropist, author and television host Jean Shafiroff hosted an elegant luncheon at Café Boulud in The Brazilian Court Hotel to honor both Women’s History Month and the work of the New York Women’s Foundation, a charity board she currently serves on and...

Rarely does a waterfront property come on the market in this desirable Southampton Shores neighborhood, so opportunity knocks for the savvy buyer who wants to reside in a Hamptons Home with extraordinary views over Wooley Pond.

Southampton Arts Center (SAC) is pleased to announce that The Robert David Lion Gardiner Foundation recently awarded a $50,000 grant to SAC to support the upcoming Museum of Democracy Exhibition, THE STORY OF AMERICA: 1776-2026, A CELEBRATION OF FREEDOM AND...

Experience the pinnacle of Hamptons living in this stunning 11,021 +/- SF contemporary masterpiece, completed in 2020. Set on a sprawling 2 acres, this estate offers an unparalleled and discerning rental experience in the Hamptons.

Perched 162 feet above sea level on one of Shelter Island’s highest natural elevations, the modern residence at 42 Prospect Avenue + Part 23 Serpentine Drive, known as “Treetops,” is recognized for both its architecture and its wide-ranging views. Built...

Over the past week, there were 30 Listings that went into contract from Westhampton to Montauk. Compared to this same week...

Read moreDetailsA masterclass in architectural restoration and design, The Van Brunt Home is a rare convergence of timeless elegance and modern...

Read moreDetailsDiscover unparalleled new construction luxury located South of the Highway in East Hampton Village at 73 Jericho Road, a prestigious...

Read moreDetailsThis property is available for the US Open this year. Private and quiet, set back approximately 340 feet off Noyack...

Read moreDetailsThe Happening in the Hamptons Podcast by Saunders & Associates is a weekly discussion covering all things Hamptons — from...

Read moreDetailsLooking for a commercial property with unmatched visibility in the Hamptons? This 0.92-acre fully renovated site sits on County Road...

Read moreDetails

#hamptons #weekend #sagharbor #cooking #easthampton")

.

.

.

.

.

#shelterisland #treetops #awardwinningmodernhome #luxuryrealestate")

is currently one of the hottest East End must-sees. Being able to watch the various whales, giant bluefin tuna, marlins, hammerhead sharks, and so many other fish feeding off Montauk in phenomenal drone-captured color footage is spellbinding.

Read the full article at Hamptons.com (Link in Bio)

.

.

.

.

#empireoftheatlantic #montauk #ocean #documentary")

.

🌼 Egg Hunt for Toddlers

📅 Saturday, April 4 | ⏰ 11:45AM–12:30PM

📍 Quogue Wildlife Refuge

Ages 2–4 with a special gift—sign up early!

🌷 Easter Egg Hunt in Amagansett

📅 Saturday, April 4 | ⏰ 12PM–1:30PM

📍 Amagansett Youth Park

Bring a basket and join the fun!

🖼️ A Thousand Words: Opening Reception

📅 Saturday, April 4 | ⏰ 6PM–7:30PM

📍 The Church, Sag Harbor

Preview this spring’s photography exhibition curated by Elisabeth Biondi.

🐰 Southampton Inn Easter Egg Hunt

📅 Sunday, April 5 | ⏰ 10AM–10:30AM

📍 Southampton Inn

Stay after for a classic Easter brunch buffet!

🍳 Easter at The Hampton Maid

📅 Sunday, April 5 | ⏰ 8AM–3PM

📍 Hampton Bays

Festive brunch, Easter Bunny visit & egg hunt for kids.

🥂 Easter Brunch at Nick & Toni’s

📅 Sunday, April 5 | ⏰ 11:30AM–2:30PM

📍 East Hampton

Celebrate with a special $95 prix-fixe brunch.

Check out more events at Hamptons.com (Link in bio)

#easter #hamptons #egghunt #art #sagharbor")

#hamptons #montauk #stpatricksday #hike #concert egghunt")